PVARA NOC Process Explained for Crypto Businesses

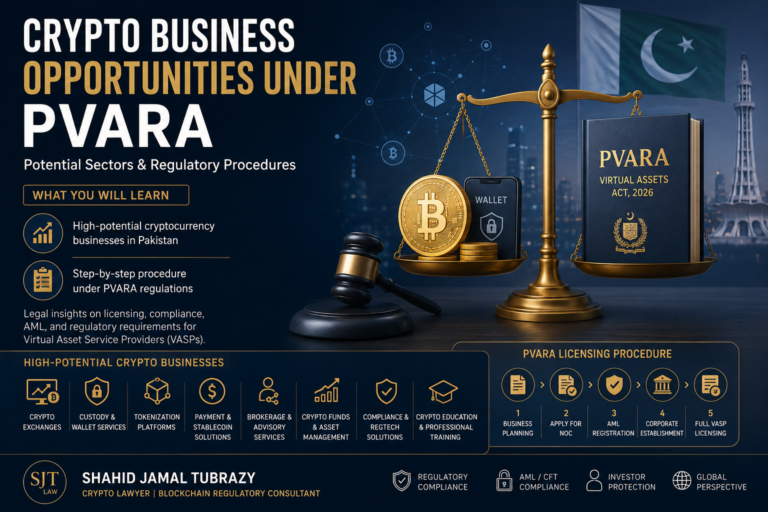

Pakistan has entered a new phase of digital asset and fintech regulation with the establishment of the Pakistan Virtual Assets Regulatory Authority and the introduction of the Virtual Assets Act, 2026. The framework is intended to regulate Virtual Asset Service Providers (VASPs), crypto exchanges, wallet providers, custodians, token issuers, brokerage platforms, and other blockchain-related businesses operating in Pakistan.

For foreign fintech and crypto companies seeking to establish operations in Pakistan, the process now requires a structured regulatory approach involving a preliminary No Objection Certificate (NOC), AML registration, local incorporation, and eventual VASP licensing under PVARA.

1. Can a Foreign Company Operate a Crypto or Fintech Business in Pakistan?

Yes. Under the emerging Pakistani regulatory framework, foreign companies may establish or expand fintech and crypto-related operations in Pakistan, subject to regulatory approval and compliance with local laws. The regime particularly targets:

- Crypto exchanges

- Virtual asset brokers

- Stablecoin issuers

- Wallet providers

- Custody providers

- Blockchain payment companies

- Tokenization projects

- DeFi infrastructure providers

- Asset-backed token projects

- Fintech remittance and digital payment systems

The primary regulator for crypto and virtual asset activities is now PVARA.

2. Is an Initial NOC Required Before Full Licensing?

Yes. According to the current framework published by PVARA Official Website, the first regulatory step is obtaining a No Objection Certificate (NOC).

PVARA clearly states that the NOC is a preliminary approval allowing the applicant to proceed toward:

- AML registration with the Financial Monitoring Unit (FMU)

- Local incorporation in Pakistan

- Final VASP licensing application

The NOC effectively serves as the gateway approval before a company can legally establish regulated crypto operations in Pakistan.

3. What Is the Procedure for a Foreign Crypto Company?

Step 1 — Preliminary Legal Assessment

Before applying, the foreign company should conduct a regulatory and legal assessment covering:

- Business model legality

- Token classification

- AML/CFT exposure

- FATF compliance obligations

- Data protection obligations

- Banking feasibility

- Corporate structure review

At this stage, engaging a local crypto lawyer is strongly advisable because the Pakistani framework is still developing and interpretation of compliance obligations remains highly technical.

Step 2 — NOC Application to PVARA

The applicant must submit a formal NOC application with supporting documentation. According to PVARA guidelines, required materials may include:

- Detailed business plan

- Corporate registration documents

- Shareholding structure

- Beneficial ownership disclosure

- Director information

- Fit & Proper declarations

- Source of funds evidence

- AML/CFT policies

- Cybersecurity and infrastructure details

- Compliance manuals

- Risk management framework

Step 3 — Regulatory Review and Due Diligence

PVARA may conduct:

- Background investigations

- Compliance reviews

- Financial capability assessment

- AML risk evaluation

- Technical infrastructure analysis

- Beneficial ownership verification

PVARA states that complete applications may be processed within approximately 30–60 business days, depending on complexity.

Step 4 — AML Registration with FMU

After receiving the NOC, the company must register with Pakistan’s Financial Monitoring Unit (FMU) and comply with AML/CFT obligations including:

- KYC procedures

- Transaction monitoring

- Suspicious transaction reporting

- Record retention

- Sanctions screening

- Compliance reporting

Step 5 — Local Incorporation in Pakistan

PVARA’s framework specifically indicates that the foreign company must establish a local Pakistani entity under the Companies Act 2017 before final licensing.

Typically, this may involve:

- Incorporating a subsidiary company in Pakistan

- Registering with the Securities and Exchange Commission of Pakistan (SECP)

- Obtaining NTN and tax registrations

- Opening local banking arrangements

- Establishing a registered office

Step 6 — Final VASP License Application

Once the above requirements are completed, the applicant may proceed toward full VASP licensing under PVARA.

4. Does a Foreign Company Need to Appoint an Executive Officer in Pakistan?

Although the current framework continues evolving, regulators generally expect foreign VASPs to appoint locally responsible managerial personnel for operational and compliance accountability.

In practice, this may include:

- A local Executive Officer

- Compliance Officer

- MLRO (Money Laundering Reporting Officer)

- Authorized local representative

- Resident director or authorized signatory

This requirement becomes particularly important for:

- AML supervision

- Regulatory communication

- Investigations

- Reporting obligations

- Enforcement cooperation

Given Pakistan’s FATF-aligned approach, regulators are likely to require identifiable responsible officers within the jurisdiction.

5. Is Hiring a Local Lawyer Necessary?

Legally, the framework may not expressly mandate a lawyer in every case. However, practically speaking, engaging a Pakistani crypto and fintech lawyer is highly advisable because:

- The framework is new and evolving

- Licensing standards are technical

- AML documentation requires localization

- Corporate structuring issues arise for foreign ownership

- Banking onboarding may require legal coordination

- Cross-border regulatory conflicts may emerge

- Tax and foreign exchange issues require local analysis

A local legal representative often assists with:

- Regulatory submissions

- Drafting policies and manuals

- Compliance reviews

- Company incorporation

- Communication with regulators

- Risk mitigation strategies

6. Important Compliance Considerations for Foreign Companies

Foreign crypto and fintech operators entering Pakistan should carefully consider:

AML & FATF Compliance

Pakistan’s framework is heavily FATF-oriented and places strong emphasis on transaction monitoring, sanctions compliance, and suspicious activity reporting.

Banking Relationships

Recent developments indicate Pakistan is gradually opening banking access for licensed crypto businesses holding a valid NOC or license.

Consumer Protection

PVARA requires operational safeguards, cybersecurity standards, and disclosure obligations.

Corporate Transparency

Beneficial ownership disclosures and Fit & Proper testing remain central requirements.

Cross-Border Operations

International exchanges and foreign fintech groups must ensure their offshore structure aligns with Pakistani licensing expectations.

7. Legal Risks of Operating Without PVARA Approval

According to PVARA guidance, operating a VASP without authorization may expose a company to:

- Regulatory penalties

- Fines

- Asset seizure

- Criminal exposure

- Banking restrictions

- Enforcement proceedings

Conclusion

Pakistan is positioning itself as an emerging regulated market for crypto and fintech businesses through the creation of PVARA and the Virtual Assets Act, 2026. The system now provides a structured pathway for foreign crypto exchanges, blockchain companies, tokenization projects, and fintech startups seeking legal market entry.

However, the framework remains in an early implementation stage. Foreign companies should approach the market with a strong compliance strategy, detailed AML controls, proper corporate structuring, and experienced local legal support.

The current pathway generally involves:

- Regulatory legal assessment

- NOC application to PVARA

- AML registration with FMU

- Local incorporation in Pakistan

- Appointment of responsible compliance personnel

- Final VASP licensing

For international crypto businesses, early legal planning and regulatory engagement will likely determine the success or failure of entering the Pakistani digital asset market.

Disclaimer

The information provided in this article is intended for general informational purposes only and should not be construed as legal or financial advice. Readers are encouraged to seek independent professional counsel tailored to their specific circumstances.

Author & Crypto Consultant

Shahid Jamal Tubrazy – Crypto & Fintech Law Consultant

Shahid Jamal Tubrazy is a recognized professional in the field of cryptocurrency and blockchain law, with specialized certification in Crypto Law from Duke University. As an experienced fintech lawyer, he provides comprehensive legal services across the digital asset ecosystem, including regulatory licensing, legal structuring for ICOs, STOs, DeFi projects, and DAOs.

He also offers expertise in crypto dispute resolution, mediation, negotiation, and mergers & acquisitions within the blockchain sector. With a strong portfolio of published work on blockchain regulation and cryptocurrency law, Shahid delivers practical legal insights to help clients navigate complex regulatory landscapes, ensure compliance, and achieve strategic growth in the evolving fintech industry.

📧 Email: shahidtubrazy@gmail.com

🌐 Website: https://cyberlawconsult.wixsite.com/cryptolawyer

📘 Facebook: https://www.facebook.com/fintechcryptolawyer

🔗 LinkedIn: https://www.linkedin.com/in/tubrazyfintechlawyer/

📝 Blogger: https://sjtubrazylegalpages.blogspot.com/